Saving money is one of the most important steps toward achieving financial stability and peace of mind. Whether you’re preparing for emergencies, planning for major life milestones, or working toward long-term goals like retirement, having a solid savings plan can make all the difference. Saving not only provides a safety net but also empowers you to make financial decisions with confidence.

If you’ve come across the keyword “gomyfinance.com saving money,” it’s a great starting point for exploring practical tools and advice to help you manage your finances effectively. Platforms like gomyfinance.com offer valuable insights and resources for individuals looking to take charge of their savings and financial future.

In this article, we’ll share actionable tips and strategies inspired by “gomyfinance.com saving money” to help you grow your savings and achieve your financial goals. From creating a budget to cutting unnecessary expenses, we’ll guide you step-by-step on your savings journey.

Let’s dive in!

Understanding Your Financial Situation

Before you can start saving money effectively, it’s essential to have a clear picture of your current financial situation. Understanding where your money is coming from and where it’s going will lay the foundation for building a successful savings plan.

Assess Your Income and Expenses

The first step is to calculate your total income. Include all sources, such as your salary, freelance work, investments, or any other streams of earnings. Once you have a clear number, it’s time to categorize your expenses. Divide them into three main categories:

- Needs: Essentials like rent, utilities, groceries, and transportation.

- Wants: Non-essential expenses like dining out, entertainment, and subscriptions.

- Savings: Money set aside for your future, such as emergency funds or retirement accounts.

This categorization helps you see where most of your money goes and identifies areas for potential savings.

Track Your Spending Habits

Tracking your daily spending is a crucial step in understanding how your habits affect your budget. By monitoring your expenses, you can pinpoint unnecessary spending and make informed decisions to reduce costs.

Consider using tools like budgeting apps or spreadsheets to simplify this process. Apps like Mint, YNAB (You Need a Budget), or EveryDollar can automatically categorize your transactions, making it easier to spot patterns. Alternatively, a simple spreadsheet can give you a customized view of your spending habits.

By regularly tracking your income and expenses, you’ll gain a clearer understanding of your financial health and be better equipped to make adjustments that help you save more.

Setting Clear Savings Goals

Saving money becomes easier and more effective when you have clear, defined goals. By distinguishing between short-term and long-term goals and using a structured approach like the SMART framework, you can create a roadmap for your financial success.

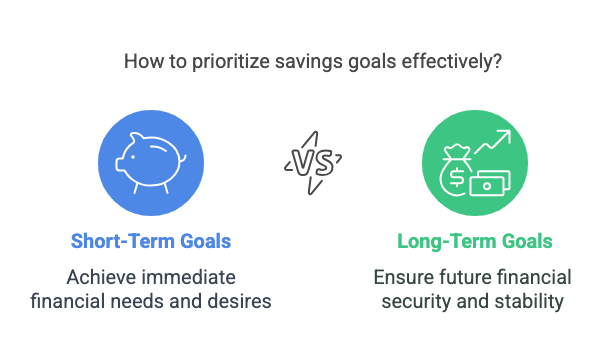

Short-Term vs. Long-Term Goals

Your savings goals can be divided into two main categories:

Short-Term Goals:

These are goals you aim to achieve within a year or two. Examples include:

- Building an emergency fund to cover unexpected expenses, such as medical bills or car repairs.

- Saving for a vacation or special event.

Long-Term Goals:

These are objectives that take several years to accomplish. Examples include:

- Saving for a down payment on a house.

- Building a retirement fund to ensure financial security in later years.

Breaking your goals into short-term and long-term categories helps you prioritize and allocate your resources effectively.

SMART Goals Framework

Setting goals is important, but they’re most effective when they’re structured and actionable. That’s where the SMART framework comes in. Here’s how to apply it to your savings goals:

- Specific: Clearly define what you want to achieve.

- Example: “Save $5,000 for an emergency fund.”

- Measurable: Ensure you can track your progress.

- Example: “I will save $500 each month until I reach my goal.”

- Achievable: Set realistic goals based on your financial situation.

- Example: “I can save 10% of my monthly income without compromising essential expenses.”

- Relevant: Align your goals with your broader financial aspirations.

- Example: “An emergency fund aligns with my goal of reducing financial stress.”

- Time-bound: Establish a deadline to maintain focus.

- Example: “I will reach my goal in 10 months.”

Using the SMART framework ensures your goals are clear and actionable, keeping you motivated and on track to achieve them.

By setting clear short-term and long-term goals using the SMART framework, you’ll create a solid foundation for saving money. This approach helps you focus on what matters most and makes it easier to stay committed to your financial journey.

Creating a Realistic Budget

A well-planned budget is the cornerstone of any successful savings strategy. It helps you manage your income, control spending, and ensure you’re consistently saving for your goals. By choosing the right budgeting method and utilizing helpful tools, you can create a realistic budget that works for you.

Budgeting Methods

There are several popular budgeting techniques that can help you organize your finances. Here are two of the most effective approaches:

The 50/30/20 Rule

This method divides your income into three categories:

- 50% for Needs: Essentials like housing, utilities, groceries, and transportation.

- 30% for Wants: Non-essentials like dining out, entertainment, and hobbies.

- 20% for Savings: Money set aside for savings goals, investments, or paying down debt.

The 50/30/20 rule is simple and flexible, making it a great option for beginners.

Zero-Based Budgeting

In this approach, you allocate every dollar of your income to a specific purpose. By the end of the month, your income minus your expenses and savings should equal zero.

- This method ensures no money is left unaccounted for and encourages mindful spending.

- It’s ideal for those who want a highly detailed and precise budget.

Both methods are effective, so choose the one that aligns best with your financial situation and preferences.

Utilizing Budgeting Tools

Creating and managing a budget is much easier when you have the right tools. Here are some recommendations:

- Apps: Apps like Mint, YNAB (You Need a Budget), and EveryDollar automate expense tracking and make budgeting more convenient.

- Templates: Use customizable spreadsheets or downloadable templates to manually track income, expenses, and savings.

- Resources on gomyfinance.com: If you’ve been inspired by the keyword “gomyfinance.com saving money,” explore their resources for budgeting advice, tools, and calculators to streamline your financial planning.

By selecting a budgeting method that suits your lifestyle and leveraging tools to simplify the process, you can create a realistic budget that helps you stay on track and achieve your savings goals. A good budget isn’t just a plan—it’s a pathway to financial freedom.

Avoiding Common Pitfalls

Even with the best intentions, certain habits and decisions can derail your savings efforts. By being mindful of these common pitfalls, you can stay on track and make steady progress toward your financial goals.

Lifestyle Inflation

One of the most significant challenges to saving money is lifestyle inflation. As your income increases, it’s tempting to upgrade your lifestyle—buying a bigger house, dining out more often, or indulging in expensive hobbies. While it’s natural to enjoy your hard-earned money, unchecked lifestyle inflation can prevent you from saving effectively.

How to Avoid It:

- Commit to maintaining your current lifestyle as your income grows.

- Allocate any extra income directly toward savings or investments instead of spending it.

- Reward yourself occasionally, but make sure it fits within your budget.

Impulse Purchases

Impulse buying is another common obstacle to saving money. These spontaneous purchases, often triggered by sales or emotional decisions, can add up and strain your budget.

How to Avoid It:

- Use the 30-day rule: Before making a non-essential purchase, wait 30 days to evaluate whether it’s truly necessary.

- Create a list before shopping and stick to it to avoid unnecessary spending.

- Unsubscribe from promotional emails or apps that encourage impulsive buying.

Dipping into Savings

Savings accounts are meant for emergencies or long-term goals, but it can be tempting to dip into them for non-essential expenses. This habit can disrupt your financial plans and reduce the security your savings provide.

How to Avoid It:

- Separate your savings into distinct accounts for different goals, such as an emergency fund, travel, or retirement.

- Set up an account with limited access to make withdrawing money less convenient.

- Remind yourself of your long-term goals and the importance of preserving your savings for their intended purpose.

By staying mindful of these pitfalls and implementing strategies to overcome them, you can build and maintain healthy financial habits. Avoiding these common mistakes will not only protect your savings but also empower you to achieve greater financial success.

Conclusion

Saving money is a journey that begins with understanding your financial situation and taking actionable steps to improve it. By assessing your income and expenses, setting clear goals, creating a realistic budget, and avoiding common pitfalls like lifestyle inflation or impulse purchases, you can build a strong foundation for financial success.

Remember, small changes in your daily habits can lead to significant progress over time. Whether it’s automating your savings, using budgeting tools, or practicing strategies like the 30-day rule, every step you take brings you closer to your financial goals.

For more insights and tools to support your financial journey, consider exploring this gomyfinance.com review. It provides a comprehensive look at how gomyfinance.com can help you with budgeting and saving strategies.

Now it’s time to take action. Start by reviewing your finances, setting a savings goal, and implementing some of the tips we’ve shared. Have your own money-saving strategies or experiences? Share them in the comments below to inspire others on their journey. Your financial future is in your hands—start saving today and take control of your money!