When applying for credit, is it preferable to receive a low interest rate or a high interest rate? This question pops up often for people new to borrowing money. In simple terms, a low interest rate is better because it saves you money over time. Think of interest as the extra fee you pay for using someone else’s money. A lower rate means less extra cost, making it easier to pay back what you owe. This guide breaks it down for students and everyday folks learning about money. We’ll look at why low rates win, with easy examples and tips.

Interest rates matter a lot in places like the United States, Canada, the UK, Australia, and emerging spots like India or Brazil. They affect loans for cars, homes, or school. Lenders check your credit history to set your rate. Good credit often gets you a low rate, while poor credit might mean a high one. But always aim low – it keeps payments small and helps you stay out of debt trouble.

What Is an Interest Rate?

An interest rate is the cost of borrowing money, shown as a percentage. Lenders add it to what you borrow, so you pay back more than you took. For example, borrow $1,000 at 5% interest for a year, and you owe $1,050. At 15%, it’s $1,150. That’s a $100 difference!

Rates come in two main types: fixed and variable. A fixed rate stays the same, so payments don’t change. A variable rate can go up or down with the market, which adds risk. What is a danger of taking a variable rate loan? If rates rise, your payments jump, making it hard to budget.

Interest shows up in many credit types:

- Credit cards: Often high rates if you don’t pay in full.

- Personal loans: For things like vacations or fixes.

- Mortgages: Big loans for homes, where low rates save thousands.

- Student loans: Help with school, but high rates add up fast.

Understanding this builds financial literacy. It helps you make smart choices and avoid costly mistakes.

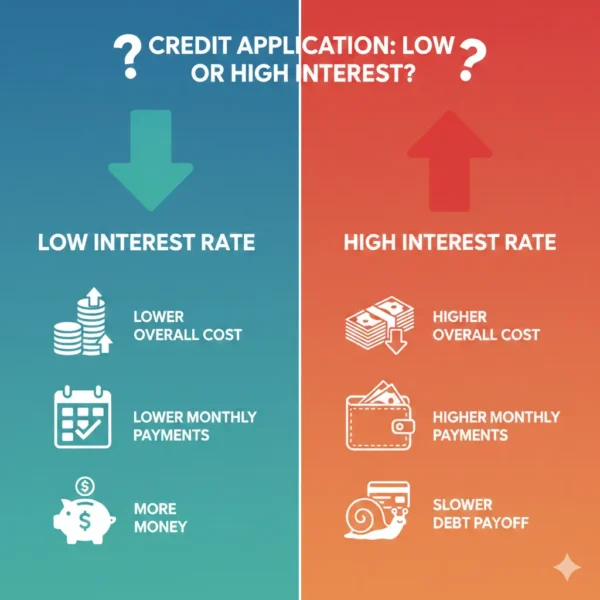

Why Choose a Low Interest Rate?

When applying for credit, is it preferable to receive a low interest rate or a high interest rate? Hands down, low is best. Here’s why:

Low rates cut the cost of borrowing. You pay less overall. For a $10,000 loan at 4% over five years, total interest might be about $1,040. At 10%, it’s around $2,700. That’s over $1,600 saved! These numbers come from basic loan calculators used in finance classes.

They make monthly loan payments easier. Lower payments free up cash for food, rent, or fun. This keeps your budget balanced and reduces stress1.

Low rates boost loan affordability. You can borrow more without straining your wallet. Banks see you as less risky, too, which helps your creditworthiness.

High rates have downsides. They raise costs and can lead to debt traps. High interest rate disadvantages include bigger payments that eat into savings. Plus, missing payments hurts your credit score more.

But why do people sometimes use credit to pay for items instead of just using cash? Credit lets you buy now and pay later, useful for big buys. Just pick low rates to keep it smart.

How Interest Rates Affect Your Loan Costs

Interest rates directly hit how much a loan costs. Let’s use real examples.

Take a car loan for $20,000 over four years. At a low 3% rate, monthly payments are about $443, with total interest around $1,264. At a high 12% rate, payments jump to $526, and interest hits $5,248. You pay over $4,000 more with the high rate!

For credit cards, say you charge $5,000 and pay minimums. At 8% APR, you clear it faster with less interest. At 22% APR, it drags on, adding hundreds in finance charges.

How does interest rate affect the total cost of a loan? It compounds – interest on interest. Low rates slow this growth. Data from the Federal Reserve shows that when rates drop, borrowing rises because it’s cheaper. In 2023, low rates helped millions refinance homes, saving an average $150 monthly.

Factors like inflation play in. High inflation pushes rates up to cool spending. But for you, focus on personal factors: your credit score and interest rates link tight. Scores above 700 often get prime rates under 5%.

Lender requirements vary. Banks want proof of income and low debt. Borrower risk assessment decides your rate – low risk means low rate.

Factors That Determine Your Interest Rate

Lenders look at several things to set your rate. Knowing them helps you prepare.

- Credit Score: High scores (670+) get low rates. Fix errors on your report to boost it.

- Income and Job: Steady pay shows you can repay.

- Debt Levels: Too much debt raises risk, hiking rates.

- Loan Type: Secured loans (like home equity) have lower rates than unsecured.

- Market Rates: Fed decisions affect all lenders.

What factors determine the interest rate on a loan application? Your history tops the list. Improve it by paying bills on time.

Sometimes lenders ask for a down payment. Sometimes lenders allow or require a down payment before they extend you the loan. This lowers their risk, often leading to better rates.

How does the bank make a profit? From interest and fees. They lend your deposits, charging more than they pay savers.

Tips to Get a Low Interest Rate

Want that low rate? Follow these steps:

- Check Your Credit: Get free reports from sites like AnnualCreditReport.com. Fix issues early.

- Shop Around: Compare lenders. Use tools like Bankrate for quotes.

- Build Credit: Use cards wisely, pay on time.

- Consider a Cosigner: What is a cosigner and what considerations should they make before co signing a loan? A cosigner with good credit helps you qualify low, but they risk if you default.

- Choose Fixed Rates: Avoid variable surprises.

- Pay Down Debt: Lower your debt-to-income ratio.

How to qualify for a low interest rate when applying for credit? Start small, like a secured card, to build history.

Avoid scams when shopping. For help, check resources on spotting fraud, like this guide on phone scams or protecting your phone number online.

Types of Credit and Interest Rates

Different credits have unique rates.

Credit Cards: High if carried over. Look for 0% intro offers, but watch post-promo jumps.

Personal Loans: Fixed rates, good for debt consolidation. Personal loan interest guidance: Aim under 10%.

Mortgages: Long-term, so low rates save big. Mortgage interest rates average 6-7% in Tier 1 countries.

Installment Loans: Like auto loans, paid in chunks. Installment loan costs rise with high rates.

What questions do you have about these different types of credit? Ask about APR (Annual Percentage Rate) – it includes fees for true cost.

Fixed vs variable interest: Fixed is safer for budgets.

Credit card interest can hit 20%+. Pay full to avoid.

For businesses, rates affect growth. But for you, focus on personal debt management.

Comparing Low and High Interest Rates

Interest rate comparison is key. Use charts:

| Rate Type | Pros | Cons |

| Low | Saves money, easy payments | Harder to qualify |

| High | Easier access | Higher costs, stress |

Choosing the best interest rate: Match to your goals. Loan terms and conditions matter – short terms with low rates cut interest.

Pros and cons of loans with low interest rates: Pro: Affordability. Con: Strict approval2.

Difference between low and high interest rates on loans: Low means less paid back.

How much money do you save with a lower interest rate? On a $100,000 mortgage, 1% lower saves $60,000 over 30 years!

How to compare interest rates from different lenders: Get pre-approvals without hurting credit.

Why do lenders charge different interest rates on credit? Based on risk.

How credit score affects interest rates on loans: Every 50-point score drop can add 1-2% to rates.

How interest rates impact personal loan repayment: Low rates speed payoff.

What to consider before accepting a loan interest rate: Total cost, not just monthly.

Is it always better to choose a low interest rate on credit cards? Yes, unless promo deals apply.

Why is a low interest rate better when applying for credit? It builds wealth faster.

For router access when checking online lenders, see this safe guide.

Common Mistakes to Avoid

Don’t rush the first offer. When applying for credit is it preferable to receive a high interest rate? No – it costs more.

Ignore fine print? Bad idea. Watch for fees.

Borrow too much? High rates amplify problems.

Use resources like this on unknown numbers to avoid scam calls from fake lenders.

FAQs

When applying for credit, is it preferable to receive a low interest rate or a high interest rate?

Low, for savings and ease.

Define principal interest term:

Principal is the amount borrowed; interest is the cost.

How can you mitigate the potential risk associated with a compressed url?

Check sources before clicking, especially in loan apps.

For more, see virtual phone numbers.

Conclusion

In summary, when applying for credit, is it preferable to receive a low interest rate or a high interest rate? Always go for low to save money, manage payments, and build a strong financial future. Low rates mean less stress and more freedom. Start by checking your credit and comparing options today3.

What are your thoughts on interest rates – have you scored a low one lately?

References

- Brainly Question on Credit Preferences – Student-focused answers with simple examples to understand borrowing costs. ↩︎

- Medium Article on Credit Interest Rates – Offers balanced pros and cons with practical tips for borrowers. ↩︎

- Quizlet Explanation on Interest Rates – Provides educational insights for students learning basic finance principles. ↩︎