In this fast-paced world, starting a business means handling finances smartly. A startup business credit card with ein only lets founders like you get funding tools without tying in personal credit. This option fits well for structured entities such as LLCs or corporations in places like the US, UK, Canada, Australia, India, and Brazil. It helps separate your personal and business money matters right from the start. We’ll dive into what these cards are, why they suit startups, how to get one, and top picks to consider.

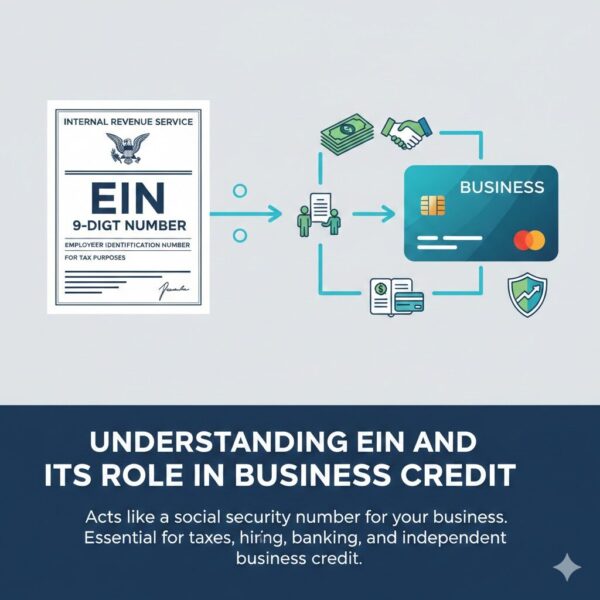

Understanding EIN and Its Role in Business Credit

An Employer Identification Number, or EIN, comes from the IRS in the US. It acts like a social security number but for your business. You need it for taxes, hiring staff, and opening bank accounts. For credit cards, an EIN lets issuers check your business’s health without looking at your personal credit score.

Many founders choose this path to protect their own finances. If your startup faces tough times, your personal assets stay safe. This setup also helps build a strong business credit history over time1. Search engines often highlight articles on this topic because they offer clear steps and real examples, making them useful for readers.

Benefits of a Startup Business Credit Card with EIN Only

Why pick a startup business credit card with ein only? It offers key perks for new businesses.

First, it keeps personal and business credit apart. This means your personal score won’t drop if business payments lag. Founders with past credit issues find this reassuring.

Second, these cards help build business credit history. Pay on time, and reports go to business bureaus like Dun & Bradstreet. Over months, this can lead to better loan terms or higher limits later.

Third, expect higher credit lines. Issuers base limits on your business revenue or bank balance, not personal income. Some cards offer up to 30 times more than standard ones.

Rewards add value too. Get cash back on office supplies, travel, or ads. For example, earn 1.5% on all spends or points for software buys.

Expense tracking gets easier. Many cards include apps for real-time monitoring, budget sets, and auto-reports to accounting tools like QuickBooks.

For startups in Tier 1 countries like the US or UK, this means smoother growth. In Tier 2 spots like India or Brazil, it aids in managing local and global costs without personal risk.

Statistics show promise: Businesses using corporate cards see 20-30% faster expense processing, per industry reports. This frees time for innovation.

Who Should Get a Startup Business Credit Card with EIN Only?

Not every business fits. These cards suit specific types.

Startups or early-stage companies with structured entity like LLCs, corporations, or partnerships shine here. Sole proprietors often miss out because issuers want formal setups.

If your venture has some revenue, cash flow, or a business bank balance—even modest—this helps. Issuers look at business activity, not personal credit.

Founders aiming to separate business and personal credit benefit most. Protect your score and limit liability.

Businesses with recurring costs, like payroll or subscriptions, find these useful. They provide a line for ongoing needs.

Those planning to build business credit history separately can access bigger financing later under the business name.

In short, if you’re a founder in a registered entity with basic financials, this card type boosts your startup funding tools.

Requirements for Getting Approved

Getting a startup business credit card with ein only isn’t automatic. Meet these basics.

Have a valid EIN. Apply free on the IRS site if you don’t.

Your business must be a corporation, LLC, or similar—not a sole proprietorship.

Show proof of activity: Revenue, bank statements, or sales data from platforms like Shopify.

Some need minimums, like $25,000 in a business account or $5,000 monthly spends.

No personal credit check happens, but expect business verification.

For international founders in Tier 2 countries, US-based operations or residency might apply for some cards.

Tips: Keep records clean. High revenue helps, but even modest cash flow works for certain issuers.

Step-by-Step Guide: How to Apply for a Startup Business Credit Card with EIN Only

Ready to apply? Follow these steps for success.

1. Get Your EIN. Visit the IRS website. Fill out Form SS-4 online. It takes minutes. Provide business name, address, and structure.

2. Research Options. Look for corporate cards that accept EIN only. Check sites like Ramp or Nav for lists.

3. Gather Documents. Have EIN, business name, registration date, revenue proof, and contact info ready.

4. Submit Application. Go to the issuer’s site. Enter EIN in the spot for it. Skip SSN fields. Upload bank statements if asked.

5. Wait for Approval. Many decide fast—within days. Some verify instantly.

6. Activate and Use. Once approved, set up the card. Link to your accounting for smooth tracking.

This process builds EIN only credit card approval confidence. For startups with little revenue, highlight any funding or sales history.

Top Startup Business Credit Card with EIN Only Options

Several cards stand out for new businesses. Here’s a breakdown.

- Ramp Card: Great for startups. No annual fee. Earn 1.5% cash back. Limits based on revenue—up to 30x standard. Needs a $25,000 bank balance. Integrates with tools for business expense management.

- Stripe Corporate Card: Suits e-commerce ventures. 1.5% cash back. No fees. Invite-only, but easy if you use Stripe. Perfect for a corporate card for early-stage business.

- BILL Divvy Card: Flexible lines from $1,000 to $5M. No hard checks. Rewards points. Requires $20,000 balance. Ideal for bad personal credit.

- Brex Card: For funded startups. Up to 7x rewards. Custom limits. May need SSN for regs but not underwriting.

- Rho Card: 1.75% cash back. No guarantee. High minimums like $50,000 balance.

Compare in this table:

| Card | Cash Back | Min Balance | Best For |

| Ramp | 1.5% | $25,000 | General startups |

| Stripe | 1.5% | None (invite) | Online sales |

| BILL Divvy | Points | $20,000 | Flexible lines |

| Brex | Up to 7x | Varies | Venture-backed |

| Rho | 1.75% | $50,000 | Growth firms |

These help with business credit card for LLC needs.

Building Business Credit with Your Card

Use your card wisely to strengthen credit.

Pay bills on time—always. This reports positively2.

Keep utilization low: Under 30% of limit.

Monitor reports from bureaus like Experian Business.

Over time, this leads to financial independence for startups. Regular use on vendors or ads builds history fast.

Example: A tech startup used Ramp to pay software subs. In six months, their business score rose, unlocking a bigger loan.

Tips for EIN Only Credit Card Approval

Boost chances with these.

Show Strong Financials. Even modest revenue counts. Link bank accounts early.

Choose the Right Structure. Form an LLC if needed—it’s simple online.

Avoid Common Pitfalls. Don’t apply as a sole proprietor. Check terms for business credit card without SSN3.

Integrate Tools. Use cards with apps for business banking for startups.

For Tier 2 founders, consult local rules on US cards.

Avoiding Financial Scams When Applying

Stay safe online. Scams lurk in finance apps. For help, check resources on spotting frauds. Learn about spotting and reporting phone scams. If you get odd calls during setup, verify like with 8443307185 or 1-8136693601. Resources cover virtual phone numbers and protect your phone number online. See guides on numbers like 4808037616 or 5104799266. This keeps your startup finance credit card process secure.

FAQs on Startup Business Credit Card with EIN Only

How to get a business credit card with EIN only for a startup?

Follow steps: Get EIN, research, apply with business proof.

Best EIN only credit card for new LLC?

Try Ramp or BILL for ease.

Startup business credit card that doesn’t require personal credit?

Yes, corporate ones like Stripe.

Business credit cards for startups with little or no revenue?

Look for those using bank balances.

Corporate credit card for startups with EIN only?

Brex fits well.

Small business credit card application with EIN?

Online forms focus on business data.

Top business credit cards for early-stage startups?

Ramp and Brex top lists.

EIN only business credit card approval tips?

Highlight revenue and keep docs ready.

Conclusion

A startup business credit card with ein only empowers founders to grow without personal risks. It separates finances, builds credit, and offers tools for success. Whether in the US or emerging markets, choose wisely based on your needs. With options like Ramp and Brex, startups gain an edge. What challenges do you face in getting business credit—share below to start a discussion?

References

- Nav’s EIN Business Credit Card Info – Focuses on building credit without SSN. ↩︎

- Startup Savant’s How-To on EIN-Only Cards – Step-by-step application tips. ↩︎

- Ramp’s Guide to Business Credit Cards with EIN Only – Detailed on benefits and top cards for startups. ↩︎