Starting a business is exciting, but getting funding tools can be tough without a credit history. That’s where startup business credit cards with no credit come in. These cards help new founders handle expenses, track spending, and even build business credit over time. If you’re a solopreneur, freelancer, or running an early-stage startup with little revenue, these options skip traditional credit checks. They look at your cash flow or bank deposits instead. In this guide, we’ll cover the best choices, how they work, and tips to get started. We’ll focus on solutions for businesses in Tier 1 countries like the US, UK, Canada, and Australia, plus Tier 2 markets such as India and Brazil where similar fintech tools are growing.

Many new businesses struggle because banks demand strong personal or business credit scores. But cards designed for startups use different rules. For example, they might approve you based on your business bank account balance or sales data from platforms like Stripe or Shopify. This makes them perfect for bootstrapped operations or those just turning profitable. Let’s dive into why these cards fit your needs and how to pick the right one.

Why Startups Need Credit Cards Without Credit Checks

Early-stage businesses often lack the credit history that big banks require. Traditional cards might ask for a personal guarantee, tying your own credit score to the business. This can be risky if things go wrong. Startup business credit cards with no credit solve this by focusing on other signals, like your revenue or cash reserves.

Think about a new e-commerce store or SaaS company. You have sales coming in, but no long track record. These cards let you pay for ads, software, or supplies without dipping into personal funds. Plus, many report payments to business credit bureaus, helping you build a score for future loans.

Statistics show the challenge: Over 70% of small businesses in the US rely on credit cards for expenses, but approval rates drop for those under two years old (source: Federal Reserve Small Business Credit Survey). In the UK, similar issues affect startups, with fintech rising to fill the gap. For Tier 2 countries like India, options are expanding through apps that link to bank accounts for quick approvals.

Key benefits include:

- No personal credit pull: Keeps your personal score safe.

- Flexible limits: Based on your business’s cash flow.

- Expense tools: Built-in tracking and controls for teams.

- Rewards: Cash back or perks on everyday spends.

One founder shared on forums: “As a new business, we needed something simple without credit hassles. These cards let us focus on growth.” This mindset matches many in our target audience—early founders wanting separation between personal and business finances.

Top Startup Business Credit Cards with No Credit Options

Here are some standout startup business credit cards with no credit checks. We’ve picked these based on ease of access, features, and user feedback. They suit very early-stage startups, solopreneurs, and small teams with revenue but no credit history1.

Ramp Corporate Card

Ramp stands out for startups. It skips personal credit checks and guarantees. Instead, it looks at your business bank account (needs at least $25,000) and EIN. If you use Stripe, Shopify, or Amazon, connect those for faster approval based on sales history.

Features:

- Unlimited virtual and physical cards.

- Real-time spend controls and alerts.

- Automated receipt capture and accounting integrations (QuickBooks, Xero).

- 1.5% cash back on all purchases.

- Partner perks worth over $350,000, like discounts on AWS or HubSpot.

Pros: High limits (up to 30x traditional cards), no fees, builds business credit by reporting to bureaus like Experian.

Cons: Not for sole proprietors; needs US-based LLC or corp. Limits can adjust if revenue drops.

For a new SaaS startup in Canada or Australia, Ramp’s tools help manage ad spends without debt risks. In India, similar fintechs are emerging, but Ramp focuses on US for now.

Stripe Corporate Card

If you process payments through Stripe, this is a great fit. No credit check—just your Stripe account history and revenue. It’s invite-only but easy if you’re active on the platform.

Features:

- 1.5% cash back, applied to your balance.

- Integrates directly with Stripe for tracking.

- No fees; pay in full monthly.

Pros: Simple for e-commerce or agencies; helps with vendor payments.

Cons: Limited to Stripe users; no physical card options in some areas.

A freelancer in the UK might use this for software subscriptions, building credit without personal ties.

Nav Prime Card

Nav offers a no-credit-check card tied to your bank account. Pay $49.99 monthly for access, with daily autopay from deposits.

Features:

- Reports to business credit bureaus.

- Includes free credit reports.

- No deposit needed.

Pros: Builds credit fast; good for bootstrapped businesses.

Cons: Monthly fee; no rewards.

Ideal for small e-commerce in Brazil, where credit building is key for growth.

OpenSky Secured Visa Credit Card

This secured option requires a deposit ($200–$3,000) that sets your limit. No bank account or credit check needed.

Features:

- Reports to personal credit bureaus.

- Upgrade to unsecured after good use.

- Accepts non-traditional payments.

Pros: Easy entry for solopreneurs.

Cons: Annual fee; no business-specific tools.

In Tier 2 markets like India, secured cards like this help freelancers start.

BILL Divvy Corporate Card

Divvy uses a soft credit check (no impact) but bases approval on business financials, like $20,000 in your account.

Features:

- Custom spend limits by team.

- Expense tracking with receipts.

- Credit lines up to $5 million.

Pros: Great for scaling teams; integrates well.

Cons: Soft check might deter some.

For agencies in Australia, this offers control over vendor services.

These cards target businesses needing expense management. For example, a startup using SaaS tools can set limits per employee, reducing risks in volatile cash flows2.

How to Apply for Startup Business Credit Cards with No Credit

Getting approved is straightforward. Follow these steps:

- Gather basics: EIN (or equivalent in your country), business bank account, proof of revenue.

- Link accounts: Connect to platforms like Stripe for instant reviews.

- Meet minimums: Aim for $5,000–$25,000 in the bank or consistent sales.

- Apply online: Most decisions are instant.

- Use wisely: Pay on time to build credit.

Tips: Check for US focus if you’re in Tier 1; look for local alternatives in Tier 2, like Razorpay in India. Avoid overspending—many are charge cards requiring full payment.

Building Business Credit with These Cards

One big plus is credit building. Cards like Ramp report to Dun & Bradstreet and Equifax. Pay on time, and your score improves, opening doors to bigger loans.

Strategies:

- Start small: Use for recurring bills.

- Monitor reports: Nav includes free checks.

- Scale up: As revenue grows, limits increase.

In the US, building credit can boost approval odds by 50% for future funding (per Nav data). Similar in the UK with bureaus like Experian.

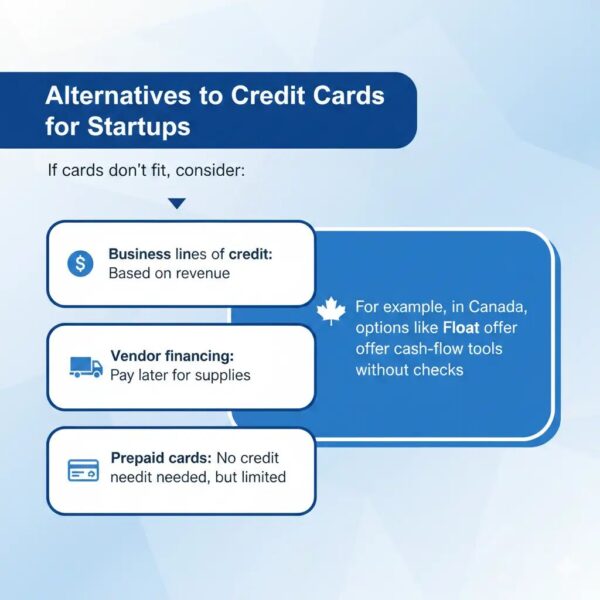

Alternatives to Credit Cards for Startups

If cards don’t fit, consider:

- Business lines of credit: Based on revenue.

- Vendor financing: Pay later for supplies.

- Prepaid cards: No credit needed, but limited.

For example, in Canada, options like Float offer cash-flow tools without checks.

Common Challenges and Solutions

New founders worry about denials. Solution: Build cash reserves first. Volatility? Choose flexible limits.

Quote from a user: “We switched to Ramp and saved on fees while tracking everything easily.”

FAQs

What are the best startup business credit cards with no credit for freelancers?

Options like Stripe or OpenSky work well, focusing on your gigs without personal guarantees.

Do these cards require revenue?

Most need some cash flow or bank balance, but secured ones like OpenSky don’t.

Can I use them internationally?

Yes, but check fees. Ramp works in Tier 1 countries seamlessly.

How do they build credit?

By reporting payments to business bureaus.

Are there no-deposit options?

Yes, like Nav Prime or Ramp.

For more on protecting your business, see our guide on spotting and reporting phone scams.

Conclusion

In summary, startup business credit cards with no credit are game-changers for early-stage businesses. They provide access to funds, expense controls, and credit-building without traditional barriers. Whether you’re a solopreneur in the US or a small team in India, options like Ramp, Stripe, and Nav make it possible. Start by checking your bank setup and applying today to fuel your growth.

What challenges have you faced getting business credit? Share in the comments!

SEO Tags: startup business credit cards with no credit, best startup business credit cards with no credit, business credit cards for startups, no credit check business cards, secured business credit cards3.

References

- Top Business Credit Cards for Startups with No Credit History – Nav – Details on cards like Nav Prime for credit building, targeting new businesses without history. ↩︎

- No Credit Check for Startups – Ramp Blog – Explains cash-flow underwriting, Ramp features, and alternatives like Stripe for revenue-based approvals. ↩︎

- Reddit Thread on Best Business Credit Cards – User insights on options like Chase and Ramp for young B2B startups. ↩︎